October 28, 2021

Industry Update by Peter Colley, National Research Director

How well things are going for the coal industry now seems to depend entirely on what timeframe you choose. Right now, loads of money are being made with coal prices through the roof. But for the longer term, organisations like the Reserve Bank of Australia and the Business Council of Australia – along with the Federal Government’s ‘Net Zero’ plan – are openly canvassing the decline of not just coal power, but also coal exports.

The Federal Department of Industry has an Office of the Chief Economist (OCE) that issues forecasts for minerals and energy every three months. Their 2 year forecast issued in late September has revised upwards the expected earnings for Australian coal – quite considerably.

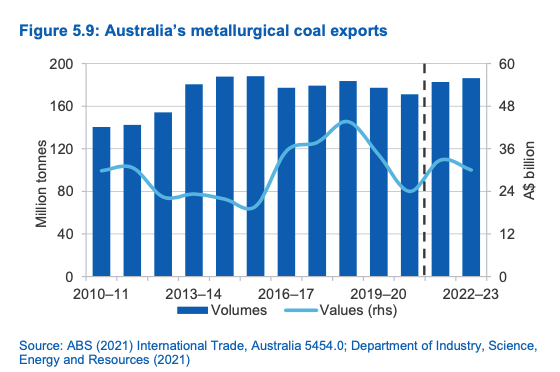

For 2021-22 the export earnings of the coking coal industry jump to $32.8 billion from $23.4b in 2020-21. That’s even though volumes increase only a little – to 183m million tonnes. Thermal coal export volumes increase a bit more – from 192mt to 208mt, while the earnings jump a lot more – from $16b to $24b.

That’s almost $57 billion in total – up with the previous peaks. It’s being driven by very high coal prices – up to US$250 per tonne for thermal coal on the spot market, and over US$400 per tonne for coking coal on the spot market. The high prices are being driven partly by the market convulsions caused by China’s ban on Australian coal, and partly by over-reliance in Europe and north America on gas and wind energy. It seems that the coal divestment push has raced ahead of the actual decline in demand for coal.

The export boom is not expected to last. The OCE has thermal coal dropping fastest in 2022-23 – down $5 billion, while coking coal drops $3b. Still, loads of money being made right now!

But the mainstream – media, business and govt – are all increasingly forecasting or canvasing the impending decline of the coal industry. And not just domestic coal power, but export coal as major customers like Japan, China and Korea all commit to reaching net zero emissions from 2050 or 2060.

Now, Scott Morrison – with the support of Nationals leader Barnaby Joyce – has also signed Australia up for net zero greenhouse gas emissions by 2050 as he heads off t0 the COP26 global climate talks in Glasgow. The 129-page ‘plan’ released by the government is light on detail about how Australia will achieve this target but its economic analysis does forecast a decline in thermal coal.

The Business Council of Australia – which has had a history of lobbying against most action on global warming – has also now embraced the target of net zero emissions by 2050, and also a steep earlier target of 46-50% reduction by 2030 – less than a decade away.

The industry that takes the biggest hit to achieve this is coal power generation – down over 60% within a decade. Coal power gets hit the hardest of all industry because the alternative technologies are already commercially available. Other industries are far more difficult to “decarbonise”.

Interestingly, the BCA acknowledges that coal mining region workforces and communities will be adversely affected and calls for a “National Regional Transition Taskforce” to focus on reducing those adverse impacts.

The Reserve Bank – hardly a bastion of green ideology – has taken to publishing scenarios that include the coal industry shrinking by over 80% by 2050. See below:

The scenario that is “Nationally Determined Contributions” is based on the current commitments of governments around the world to reduce their emissions. That is, if governments do what they say they are going to do. This scenario has Australian coal exports declining slowly to about 2030, and then rapidly. We should also note that the two further scenarios – the ones that actually keep global warming to 2 degree or less – have Australian coal exports declining more rapidly.

The Reserve Bank doesn’t think the decline in coal exports will have a huge impact on the national economy – it expect other exports to take their place. But it also says that it is coal mining regions that will be hurt, and implicitly that is where public policy action should be directed.

The Federal Government’s net zero plan makes lots of reference to support for regional areas, but little detail about what that looks like.

So should we “make hay while the sun shines” or brace for “winter is coming”? We should do both!